In the recent cycle, businesses are experiencing margin compression from multiple sides. Upstream, the return of tariffs and supply chain volatility are increasing input costs. Downstream, legacy pricing metrics, often established during periods of market stability, lack the flexibility to capture value as market conditions shift.

When margins compress, the standard response is to audit price points: a 5% increase across all tiers, a blanket rate adjustment, a renegotiated contract ceiling. This approach exacerbates existing structural flaws, requires active upselling, and is difficult to pitch once customer relationships have been established.

The better lever to pull is re-structuring the pricing metric itself.

The fundamental problem with misaligned pricing metrics is that companies end up overcharging light users and undercharging power users simultaneously. Consider an AI provider charging $200 per seat for a power user who is consuming $5,000 worth of backend compute. The light user finds the product too expensive to justify. The power user overloads the system. Both would likely accept better-defined pricing if the business can clearly show how each customer benefits from the structure. In many cases, providers are knowingly subsidizing their most active customers, tolerating it because the perceived value of the service is evolving faster than the pricing model.

Correcting the pricing metric is not about penalizing customers. It is about establishing a frictionless exchange of value. When done correctly, it enables:

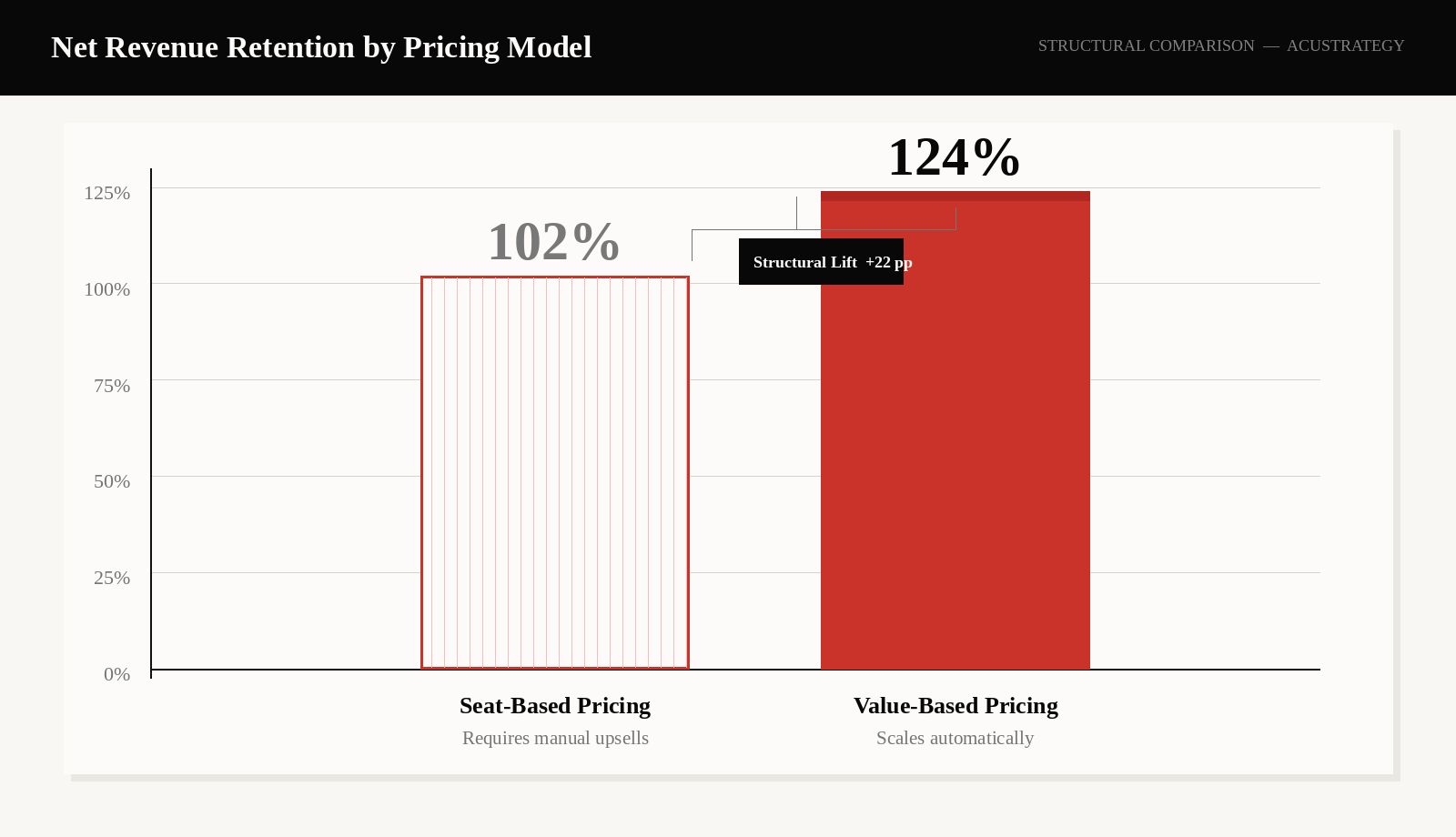

- Seamless Expansion: When the pricing metric tracks results like revenue processed, active campaigns, or shipments delivered, NRR expansion happens automatically without a sales intervention.

- Reduced Churn at the Low End: Misaligned metrics frequently force smaller customers to overpay relative to the value they receive, which accelerates churn. A true value metric lowers the barrier to entry and allows providers to capture the long tail of the market.

- Structurally Sound NRR: By right-sizing power users, providers eliminate the hidden subsidy that caps revenue growth and allow NRR to scale in proportion to the value delivered.

Trap 1: Per-seat models penalize NRR

When a company charges per seat, the product rarely achieves company-wide adoption. Instead of becoming embedded across an organization, it gets allocated to a handful of specialists. The license becomes a rationed resource rather than an operational standard.

This dynamic creates four distinct forms of revenue leakage

Usage atrophy

By limiting the number of licensed users, the customer constrains adoption to a subset of their team. The product operates as a specialist tool rather than achieving the company-wide entrenchment that would make it difficult to replace.

Shallow integrations

With fewer users, the product develops fewer connections to adjacent workflows. Lower integration depth means lower switching costs and a much easier path to cancellation during a budget review.

The sharing subsidy

Clients share login credentials to avoid incremental seat costs. The provider absorbs the infrastructure and support burden of multiple users while capturing revenue from only one. Alternatively, organizations route tasks through licensed employees, slowing execution and reducing the visible ROI of the product.

Mispriced power users

If the top 5% of customers account for 50% of total activity but pay the same as the median user, the provider is effectively subsidizing its most successful customers. This creates a hard ceiling on NRR. To grow those accounts, a sales team must negotiate an upsell rather than revenue expanding naturally alongside the client’s growth.

Customers using per-seat models often overlook the misallocation. Cost structures are centralized and teams rarely have KPIs tied directly to usage efficiency. The misalignment goes unexamined during growth periods. When growth slows and optimization initiatives begin, the structure comes under real scrutiny and the provider is exposed.

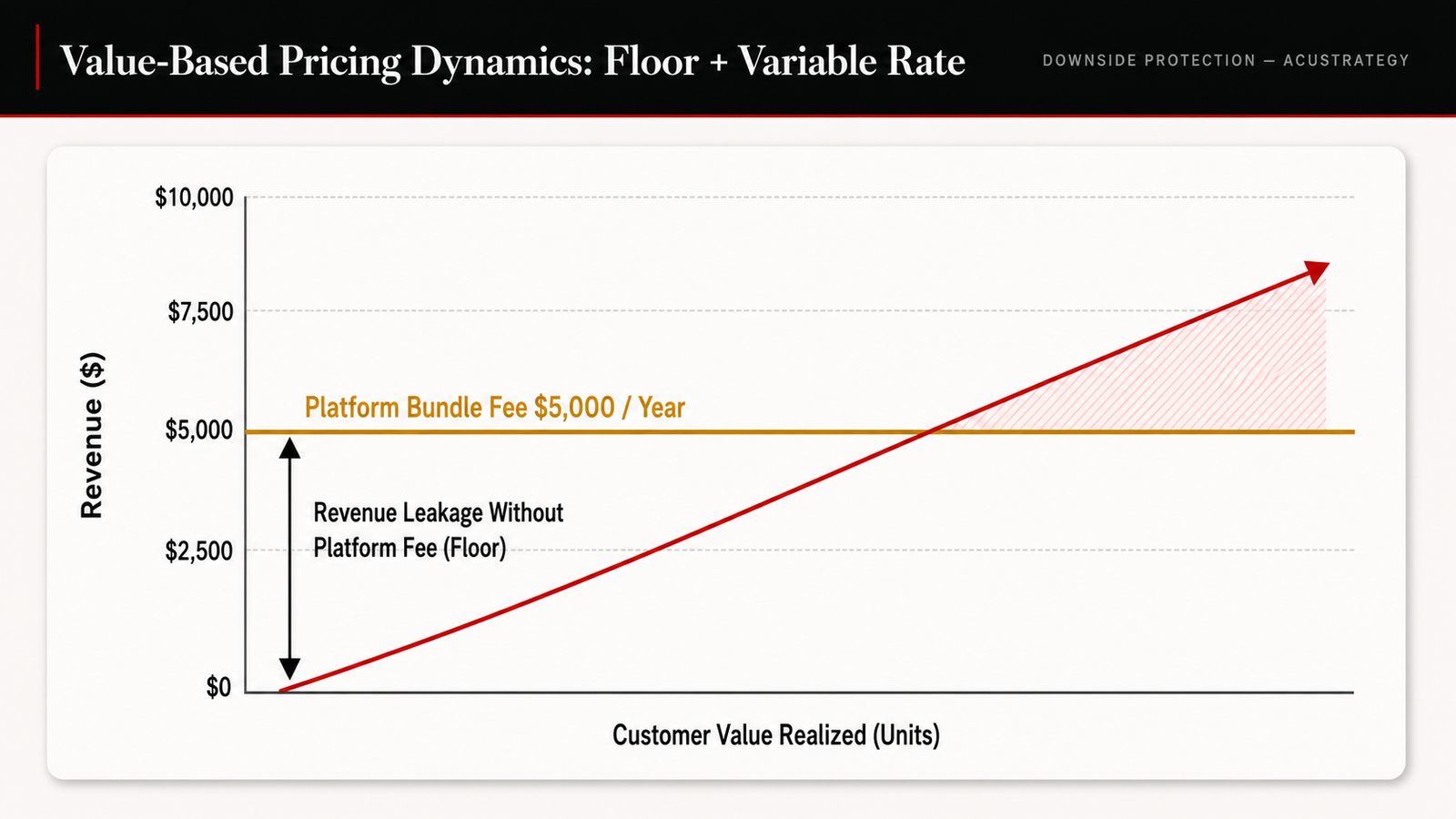

Solution: Value-based pricing (floor + variable rate)

To remove this friction, providers transition to metrics that scale with results. This repositions the provider from a cost center to a growth partner. When pricing aligns with business outcomes, increased usage is directly tied to the customer’s own revenue growth, making the case for a higher rate significantly easier to justify on both sides of the table.

The principle is straightforward: instead of charging for the operator, charge for the result.

- Logistics: Charge per shipment delivered, not per dispatcher seat.

- Marketing: Charge per qualified lead, not per marketing seat.

- Finance: Charge per invoice processed, not per accounting user.

- Customer Support: Charge per resolved ticket, not per support employee.

The pattern holds across industries. The specific metric changes; the logic does not.

To mitigate the risk of the provider absorbing costs from a customer’s operational failures, a base platform fee is established alongside the variable success rate. A logistics platform might charge a $5,000 annual base plus a rate per shipment completed. This structure allows the provider to cover fixed infrastructure costs while ensuring that revenue scales with the customer’s success.

The results-based metric also provides a natural hedge against inflation. Revenue adjusts dynamically as the customer’s activity grows, without requiring active renegotiation.

Downside protection: Leadership must account for stagflation risk. In a stagflationary environment, price increases may be accompanied by a contraction in volume. A purely variable metric in that scenario could cause provider revenue to decline if client volumes fall. This is why the floor is not optional. It protects the provider during volume contractions, while the variable rate captures the upside during growth cycles. Both components are structurally necessary.

Pricing & growth expertise

Expert-led pricing & growth strategy for growth-focused and PE-backed companies.

Enterprise-quality work. Practical recommendations. 6-10 week timelines.

Trap 2: Neglecting operational synergy

Many companies define pricing metrics based on internal cost structures: usage minutes, API calls, compute cycles, or storage consumed. This cost-plus approach is intuitive from an engineering standpoint, but it fails to capture the actual value delivered to the customer and it systematically underprices the most valuable use cases.

A tool that saves an enterprise 10,000 hours per month generates second-order effects well beyond those hours. If a platform breaks down silos, fosters cross-functional collaboration, or creates a single source of truth, it becomes more valuable as adoption expands. This is operational synergy: the point at which the total cost of ownership (TCO) becomes lower than the sum of individual efficiency gains. Customers experience it as decreased administration overhead, reduced operational friction, and higher team velocity.

At a technical level, operational synergy is enabled by anything that reduces system complexity, whether automating the slowest parts of a team’s workflow or solving genuinely difficult problems that require specialized capability. Practically, this includes team-level workflow automations, live collaboration features, SLA guarantees, SSO, compliance exports, and advanced integrations with the customer’s existing stack.

When providers price purely on internal cost metrics, they leave the synergy value entirely on the table and give customers no pricing signal that the enterprise tier delivers qualitatively different value.

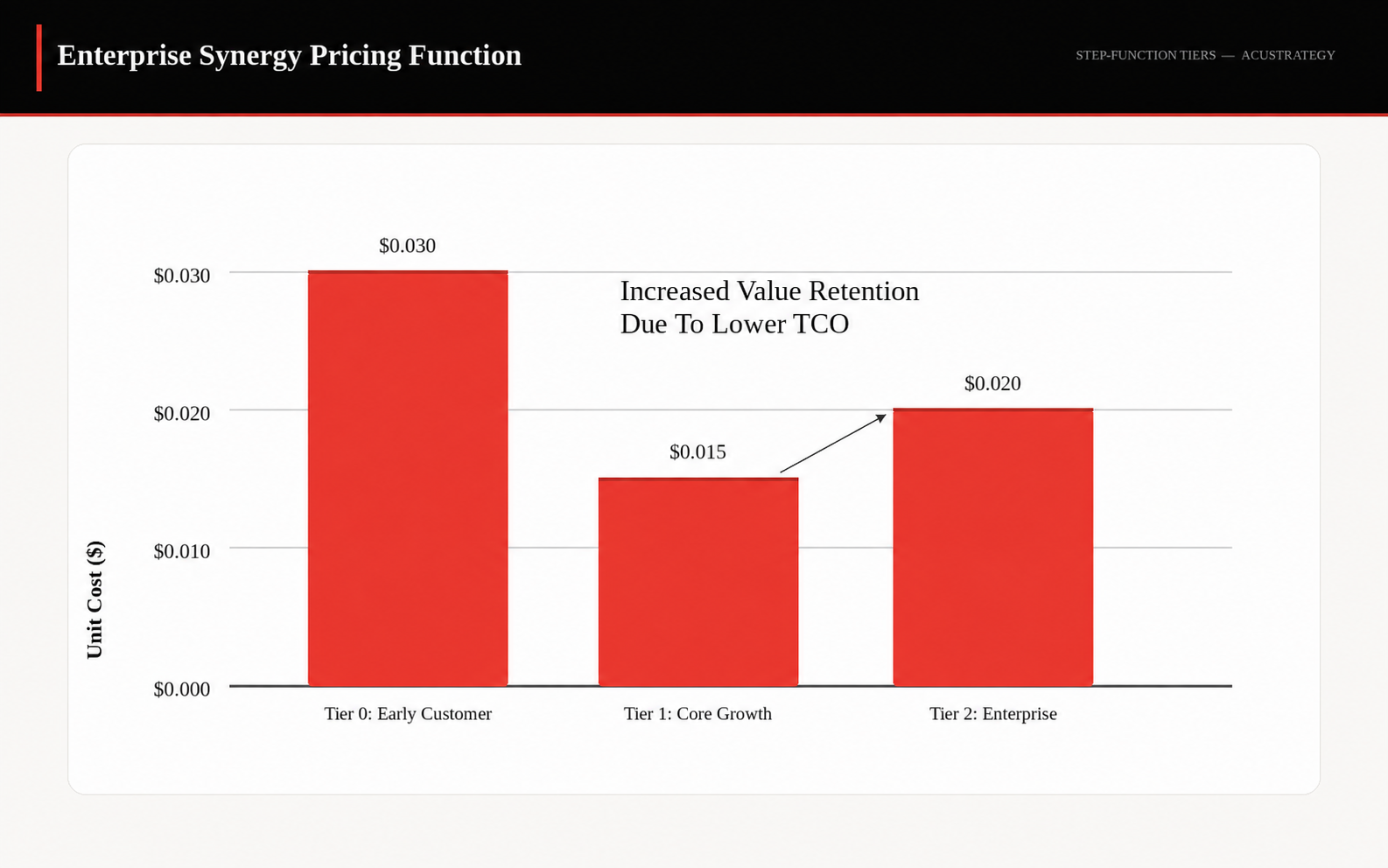

Solution: Step-function tiers

Rather than linearly metering usage, per-usage metrics are packaged into tiers based on the total value delivered at each level of operational complexity. Customers scale their usage but purchase the bundle that matches where they actually are, not a proportional extrapolation of a base rate.

This solution requires three conditions: a sticky service, a niche or technological moat, and a favorable customer relationship. When these conditions are not met, providers must price in the risk of competitive displacement, which compresses available margin. When they hold, the effective unit cost can legitimately increase at higher tiers because the integrated value of the enterprise feature set reduces the customer’s TCO more than any lower-cost alternative could.

Here is an illustrative scenario:

- Tier 0 (The Anchor): $30 per 1,000 transactions. Effective unit cost: $0.030. This tier serves as a baseline, allowing early-stage customers to test the platform with minimal commitment. It is intentionally simple and intentionally limited.

- Tier 1 (Core Growth): $1,500 per month for up to 100,000 transactions, including 80% of the feature set. Effective unit cost: $0.015. This tier captures the majority of the market (>80%), delivering the core functionality that enables growth without requiring enterprise-grade infrastructure.

- Tier 2 (Enterprise): $4,000 per month for up to 200,000 transactions. The effective unit cost increases to $0.020, a 33% premium over Tier 1. Overages are billed at $0.02 per unit. This tier unlocks the portions of the feature set that enable cost synergy: deep integrations, compliance tooling, SLA guarantees, and workflow automation.

At the enterprise tier, the provider is not selling volume. They are selling a reduction in TCO. Procurement teams are conditioned to expect volume discounts at scale. The step-function model reframes the conversation: the enterprise customer accepts a higher per-unit rate because the incremental value of the enterprise feature set generates cost savings that exceed the pricing premium. Splitting those savings with the provider is a straightforward value exchange, provided the math is made explicit.

Key consideration: pricing the customer relationship

Pricing strategy does not operate in isolation from the customer relationship. A technically correct pricing model deployed without regard for customer context will underperform and in the worst case trigger churn and reputational damage that outlasts the revenue it was designed to protect.

Providers must have a clear understanding of where they stand in the relationship before restructuring pricing. Breaking an implied pricing promise does not simply cause churn. It signals operational incompetence and damages the brand in ways that are difficult to recover from, particularly in tight-knit industry verticals where reputation travels quickly.

The customer relationship defines the effective ceiling for pricing decisions. The question is whether the business is optimizing for the current contract or for the lifetime value (LTV) of the customer. The answer depends on the nature of the market.

- Optimize for the transaction when operating in a segment with naturally high turnover, where return customers are the exception. In that context, maximizing the current contract makes structural sense.

- Optimize for LTV when operating in a market with repeat customers. Here, the customer relationship is a strategic asset. Providers can leverage it to build a brand and compound gains over a longer horizon.

Both approaches still require a fair exchange of value. Negative word-of-mouth travels fast in concentrated markets, through reviews, through direct referrals, through industry conversations. No pricing strategy survives a reputation for extractive behavior in a market where buyers talk to each other.

Transitioning accounts to new pricing metrics

Implementation requires more than a new rate card. Results-based pricing must be anchored to a metric that is technically feasible for both the provider and the customer to measure, report on, and trust. That starts with analyzing the value proposition and identifying the metric that most closely tracks the outcomes customers actually care about.

When a full shift is not immediately feasible due to technical or billing constraints, a dual-track transition preserves momentum without requiring a simultaneous migration of the entire book of business:

- New Customers: Implement the new pricing metric immediately for all new contracts. This establishes the new structure as the default, builds a clean data set to refine the model, and avoids encoding legacy constraints into new relationships.

- Legacy Accounts: Rather than forcing a migration, use on-demand renegotiations. When existing clients request new features or service expansions, require a transition to the new metric as part of the upgrade. This frames the change as access to expanded functionality, not a retroactive price increase. The customer makes the decision to move; the provider makes the new structure the prerequisite for the next level of service.

The metric is the message

Revenue leakage is rarely the product of a single failed negotiation. It accumulates over time inside a pricing model that was never designed to capture the value the product actually delivers. The fix is not a price increase. The fix is a structural realignment between what customers pay for and what they receive.

Moving from fixed inputs to value-based metrics allows companies to realize meaningful margin expansion without changing the underlying product and without the adversarial dynamic that comes with a blanket rate hike. The objective is clear: stop subsidizing power users, ensure that revenue scales in proportion to the value created, and eliminate the ceiling that per-seat and cost-plus models quietly impose on NRR.

Customers do not resist paying more. They resist paying more for something that does not feel like more. When pricing is restructured around outcomes, the conversation shifts from cost justification to value sharing, and that is a position both sides can work from.

Ready to fix your pricing metric?

If your pricing is still built around seats, API calls, or cost-plus logic, the revenue leakage outlined in this article is already happening. Acustrategy works with B2B and PE-backed companies to identify the right pricing metric, design the transition, and execute the rollout without disrupting existing customer relationships.

Most engagements close in 6 to 10 weeks with measurable topline impact. Reach out to Acustrategy to see where your current pricing model is leaving money on the table.